KKR is a top holder of Ingersoll Rand, where equity grants aren’t just for the top executives.

Giving workers skin in the game makes for a better partnership. Photographer: James W. Welgos/Archive Photos/Getty Images

Over the last few months, I’ve written about how the pandemic has served to shine a light on the companies that are truly committed to environmental, social and governance improvements. I’ve also talked about how the industrial workplace is evolving, necessitating changes in the type of jobs and skills that are increasingly in demand. Today, I want to talk about a company that brings together both ideas.

In September, Ingersoll Rand Inc. issued $150 million worth of stock to its employees. Unlike at most companies, where only the top echelons of management are paid in equity, this grant was for the rank and file, some 16,000 of them, including hourly workers. The grants equated to 20% of employees’ annual base cash compensation and were incremental to what the workers otherwise would have expected to take home this year.

The company did something similar in 2017, back when it was still called Gardner Denver and private equity firm KKR & Co. was taking it public again after a 2013 buyout. When the company announced a transformational combination with Ingersoll-Rand Plc’s industrial unit in the spring of 2019, it decided to re-up the strategy so that the thousands of employees joining its ranks could benefit as well. The transaction closed on Feb. 29, just weeks before the world was turned upside down by the coronavirus pandemic. And yet, Ingersoll Rand still followed through.

The grants were issued on the same timeline as originally planned, according to Vicente Reynal, Ingersoll Rand’s chief executive officer. “We never thought about pushing it or canceling it,” he said in an interview. “We want employees to have skin in the game and a stake in the long-term shareholder value creation we expect to achieve.”

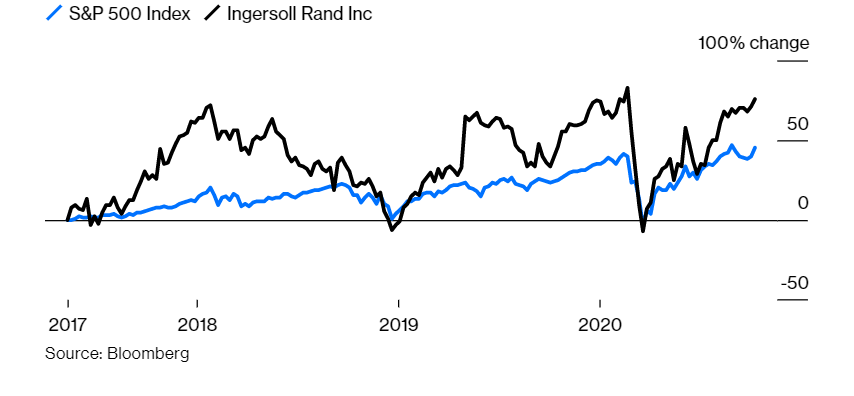

The Proof is In the Stock Price

Ingersoll Rand’s benchmark-beating gains suggest the employee equity grants are working.

The equity-grants-for-all model is the brain child of Peter Stavros, KKR’s co-head of Americas private equity and Ingersoll Rand’s chairman. Stavros’s father operated a road grader for a construction company, and his complaints about the lack of alignment between workers and management stuck with his son. Under Stavros’s leadership, KKR has now implemented this strategy at eight different companies, including pharmaceutical capsule manufacturer Capsugel, Minnesota Rubber and Plastics and aerospace hardware company Novaria. The idea is that if workers feel like they will personally benefit when the company succeeds, they’ll be more invested in things like inventory management and software enhancements.

Stavros views manufacturers as particularly fertile ground for this kind of model because there are so many levers to pull to enhance productivity (from procurement to scrap reduction and quality control) and because the hourly workforce is usually the best positioned to actually pull those levers. By contrast, there’s not as much variability in the development of software, while retailers have too much employee turnover to make this type of program worthwhile. But I don’t know of any other major manufacturers that have followed suit. Both Stavros and Reynal said they talk regularly with companies that are interested in replicating what they’ve done with equity grants at Ingersoll Rand, but that initial enthusiasm doesn’t usually translate into action.

“There’s a belief that ownership is complicated and not everyone understands it. That’s offensive to me because my dad was an hourly employee and the smartest guy I know,” Stavros said in an interview. The biggest issue may be that “treating people like owners is hard work,” he said.

It’s an enormous logistical undertaking to give equity to 16,000 people and coordinate with different regulatory regimes across numerous countries. But the grants are actually just the first step. For the ownership model to really be effective, training also has to take on a different lens. So Ingersoll Rand is working with the nonprofit Operation Hope to provide personal-finance education to its employees and Reynal himself helps conduct regular sessions to share data and brainstorm how to close performance gaps. In one example of how this has encouraged workers to speak up more and feel more engaged in the decision-making, Reynal said Ingersoll Rand received hundreds, if not thousands, of ideas from employees on ways to reduce costs as the pandemic crippled business activity. Some of those ideas have helped save jobs, he said.

To be clear, some cuts are still being made: Ingersoll Rand had already planned to trim its headcount as part of its post-merger integration. In August, it credited incremental reductions for helping the company realize $80 million of savings this year, $10 million more than previously targeted.

“Capitalism does result in changing competitive dynamics,” Stavros said. “How does that translate and interface with, ‘Ok, you said you care about employees?’ Being a stakeholder capitalist doesn’t mean that you don’t do things that make the company more efficient. It’s about how you treat people.”

This strikes me as the right way to think about ESG and stakeholder value. It’s not black-and-white; it’s unrealistic to think companies are going to completely disentangle themselves from the hard-nosed world of finance. But there is room to meet in the middle and there does seem to be a growing realization among companies that things need to change.

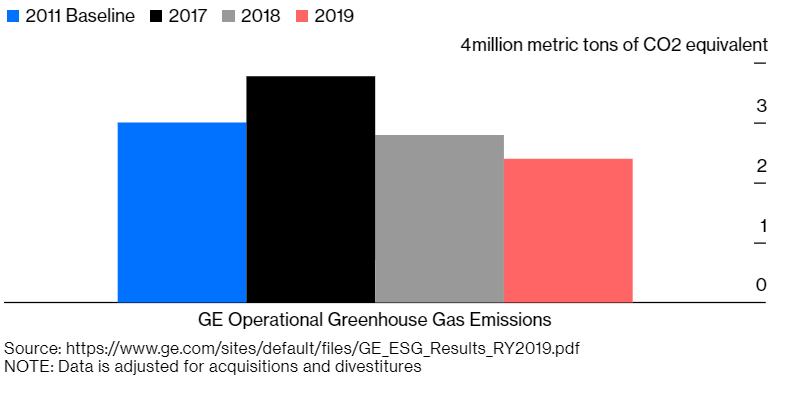

Aiming for Better

GE’s goal of becoming carbon neutral by 2030 will require a major reduction in greenhouse gas emissions

Elsewhere this week, Rockwell Automation Inc. confirmed that next month it would reverse temporary salary reductions implemented during the worst of the pandemic and reinstate matches for 401(k) retirement accounts. General Electric Co., meanwhile, announced an ambitious initiative to make its operations carbon neutral by 2030; this will entail eliminating or counterbalancing a whopping 2.39 million metric tons of carbon dioxide emissions, the equivalent of what a half million cars generate in a year. The effort builds on the company’s plan announced last month to stop selling equipment to new coal-fired power plants. I know it’s en vogue to make these fancy sustainability commitments, but it does mean something that a company like GE, whose business is still heavily linked to fossil fuels, would be willing to throw its weight behind solving the climate change challenge.

Earnings

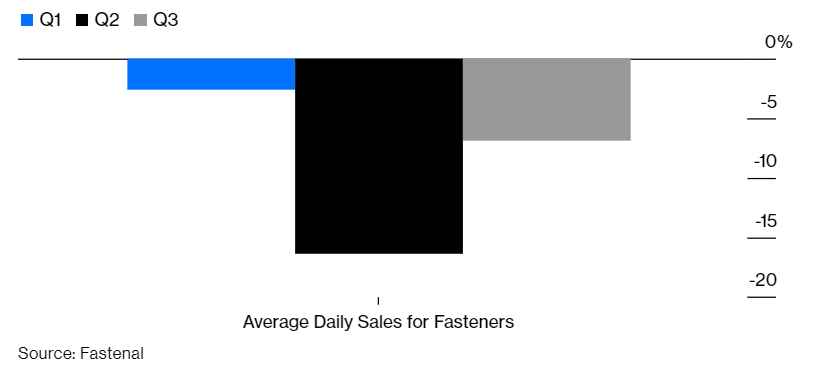

This week brought the first batch of third-quarter numbers for industrial companies. Among the notables, Fastenal Co. and Kansas City Southern provided more evidence of a recovery in general industrial markets, albeit a slow-moving one. Fastenal called out “gradual sequential improvement” each month, while Kansas City Southern raised its 2020 earnings guidance and, in a sign of confidence, announced an accelerated buyback program for $500 million of stock. One other interesting comment worth noting was that certain kinds of face coverings — particularly three-ply masks and disposable respirators — are now oversupplied, according to Fastenal. This is pressuring prices and dragging down the company’s gross margin, potentially foreshadowing headaches for 3M Co. after its aggressive ramp-up of N95 production. Too many masks is a good problem to have, though; it wasn’t that long ago companies were having to safeguard shipments from government seizure. And who knows what the future holds.

On the Mend

Industrial distributor Fastenal called out gradual improvement in its business each month as the economy recovers from the second-quarter pandemic shock

Over in the aerospace world, things remain terrible and have the potential to get worse for manufacturers and suppliers before they get better. Delta Air Lines Inc. said it was pushing out $5 billion of mostly Airbus SE plane deliveries until after 2022 and repeatedly emphasized a desire to stay “nimble” with its fleet even amid some modest improvements in travel bookings. United Airlines Holdings Inc. CEO Scott Kirby’s attempt to proclaim the current moment as a turning point for a travel recovery fell on deaf ears on Wall Street, with analysts noting its hubs cater heavily to the hard-hit corporate and international travel markets. As if to underscore the challenges ahead, Boeing Co. this week said it has now shaved a net of nearly 1,000 planes from its order backlog so far this year. The company is looking to cut costs any way it can, including apparently through a sale of its Seattle-area commercial jet headquarters. Its embattled 737 Max looks set to finally be cleared for service in Europe, although the last thing anyone needs right now is more planes.

Deals, Activists and Corporate Governance

GE may sell its nuclear turbine unit, French newspaper Le Canard Enchaine reported this week, citing an unnamed person who’s involved in talks. The French government has asked utility EDF if it’s interested in purchasing the business — which may be valued at 1 billion euros ($1.2 billion) — but the company is reluctant to do so, according to the paper. GE acquired the nuclear turbine business as part of its disastrous acquisition of Alstom SA’s energy assets. Any divestiture would fit with analysts’ speculation that GE’s power portfolio could be ripe for an unwind.

W.R. Grace & Co. was once again the subject of takeover speculation after director Kathleen Reiland resigned from the board because of disagreements over the company’s strategic direction. Reiland was added to the board last year as part of an agreement with W.R. Grace’s largest shareholder, 40 North Latitude Master Fund Ltd. Analysts said her departure may signal 40 North is preparing to take a more adversarial stance at W.R. Grace amid an uninspiring performance lately. The company often comes up as a potential target for Honeywell International Inc.

Americold Realty Trust agreed to buy cold-storage company Argo Merchants Group for $1.74 billion from Oaktree Capital Management. The deal expands Americold’s temperature-controlled warehouse assets in Europe, Australia and South America and adds key locations near ports that will help it better serve multinational customers. Cold storage is essential to the global food supply chain, something that has been in the spotlight of late amid the pandemic.

Exelon Corp. is considering splitting off its non-utility operations, which include 21 nuclear reactors as well as solar, wind and natural-gas generating assets, people familiar with the matter told Bloomberg News. This would follow similar moves by DTE Energy Co. and Dominion Energy Inc. to narrow their focus to regulated power markets and comes after activist investor Corvex Management said a breakup could help boost Exelon’s value to $60 a share, a roughly 45% premium to current levels. Bloomberg Intelligence analyst Kit Konolige expressed skepticism Exelon would find many buyers for its non-utility assets given most peers are also looking to simplify, and said the nuclear reactors may be a stumbling block for others. A spinoff may be more likely.

Traton SE, the heavy-truck unit of Volkswagen AG, agreed to acquire the shares of Navistar International Corp. it doesn’t already own for $44.50 apiece, or $3.7 billion, the company said in a statement on Friday. The transaction is supported by major Navistar shareholders Carl Icahn and Mark Rachesky’s MHR Fund Management. Volkswagen and Traton need the Navistar deal to get access to the North American market for heavy trucks and to better compete with rivals Daimler AG and Volvo AB. Friday’s agreement brings an end to months of back and forth over price.

Article Credit: bloomberg