OBSERVATIONS FROM THE FINTECH SNARK TANK

Climate change is a hot (pun intended)—and controversial—topic. While many banks are implementing environmentally friendly policies regarding their carbon impact and energy usage, a new study from Cornerstone Advisors and Meniga (written by me) demonstrates that there is a significant opportunity for banks to gain a competitive advantage by serving climate-conscious consumers.

What Banks are Doing About Climate Change

Banks aren’t oblivious to the concerns regarding climate change. A recent Accenture study found that 71% of US banks can monitor and assess their carbon footprint and two-thirds are prepared to direct capital away from the energy sector to assist in the transition to a low-carbon economy.

In addition, 62% of banks monitor clients’ emissions and environmental profiles, although many find the availability and granularity of the data insufficient to assess climate risk and the financial risk associated with evaluating lending decisions.

Banks’ climate-related activities are internal policy actions, however—they don’t directly impact consumers or have any impact on consumers’ climate-related needs.

What do Consumers Do About Climate Change? Not Much

According to Cornerstone’s survey of 3,150 US adults, nearly one in four Americans consider climate change to be the most important social challenge facing the country. No other challenge was cited by that many respondents.

Of consumers who didn’t mention climate change as the most important challenge, 44% still said they consider climate change to be a very important issue. So, overall, nearly six in 10 Americans are very concerned about climate change.

What they’re doing about it is another story.

Despite the strong concern for climate change, few consumers track their carbon footprint. In fact, among consumers who consider climate change to be the most important social challenge, just 9% track their carbon footprint. Among the rest of the population, that percentage isn’t far behind at 7%.

Why don’t consumers track their carbon footprint? They don’t know how.

You would expect consumers who consider climate change to be the most important social challenge to take action to reduce their carbon footprint, right?

Wrong. Only half of them have done so. And among the rest of Americans, only 31% said they have taken some form of action to reduce their carbon footprint.

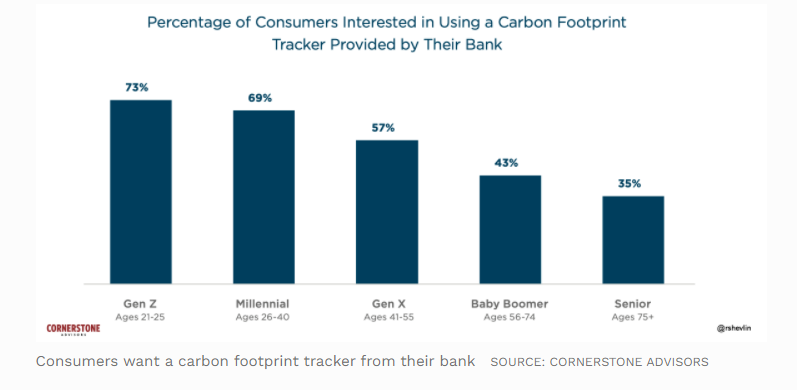

Consumers Want Banks to Help Them Manage Their Climate Impact

The good news is that many consumers want to do something about climate change. The (potentially) surprising news is that many—in particular, Gen Zers and Millennials—want help from the banks and credit unions they do business with.

Consumers Want Climate-Friendly Financial Products

Consumers want more than just a climate tracker from their bank, however. At least a third of all consumers are very interested in checking accounts with:

- Rewards for purchases made from environmental-friends

- Debit cards made from renewable or upcycled materials

- Policies that prevent deposits from funding fossil fuel exploration or production

- An option to plant a tree with every roundup

SOURCE: CORNERSTONE ADVISORS

In addition, about a third of consumers concerned with climate change say it’s important for a lender to provide green lending products like home modernization loans, green mortgages, and green car loans.

The Climate Change Opportunity in Banking

The 23% of consumers who consider climate change to be the most important social challenge hold roughly $788 billion in deposits—about 35% of all bank deposits. Their average checking account balance is nearly $14,000, 50% higher than the national average.

In addition, about one in five of them have taken out at least one loan over the past three years. These climate-conscious consumers account for 34% of the total funds borrowed, averaging nearly $110,000 per loan—roughly double the average loan size of other borrowers.

The climate change opportunity in banking isn’t limited to the 23% of consumers who are climate-conscious, however.

There’s another segment of the market: climate-aware consumers. They don’t consider climate change to be the most important social challenge, but they do consider it to be very important.

Demographically, climate-aware consumers—who comprise 34% of all consumers—aren’t as affluent as the climate-conscious group, but they’re just as interested in tracking their carbon footprint and using climate-friendly financial products as the climate-conscious consumers are.

Banks Can Compete On (Not With) Climate Change

Competing on the basis of a climate-based strategy isn’t unique. Established banks like Bank of the West and Amalgamated Bank have developed climate-based strategies, as has community bank Decorah Bank with its Greenpenny spinout.

In addition, fintechs like Atmos, Ando, and Aspiration are pursuing climate-based strategies. Who knows, maybe someday a climate-focused fintech whose name doesn’t start with the letter “a” will come to market.

The market for climate-based financial products and strategies are far bigger than just a handful of banks and fintechs can meet.

It’s not about value-signaling or pandering to a small group of Birkenstock clad tree-huggers. Climate-conscious and climate-aware consumers are mainstream consumers and there are opportunities for banks and credit unions to focus their corporate strategies around products and services to serve these consumer segments.

Article Credit: forbes